AI’s Gold Rush in Finance: Innovation, Consumer Data, and the New Risk Frontier

Context: AI in finance is moving from generic financial Q&A toward account-connected, personalized money guidance. OpenAI’s May 2026 preview of personal finance in ChatGPT, supported through Plaid ande initially available to U.S. Pro users, signals a broader shift: AI tools are beginning to connect directly with financial accounts to deliver more contextual insights.

This shift is expanding what AI can do in financial services. What began as automated budgeting and chatbot support is evolving into AI-enabled financial planning, investment explanations, fraud detection, customer engagement, and account-level analysis.

The opportunity is significant. AI can make financial services more intuitive, accessible, and proactive. Yet the same data that makes AI powerful, including transaction histories, income patterns, debt obligations, spending behavior, investment holdings, and personal goals, is also among the most sensitive information a consumer can share.

The real question is no longer whether AI has a role in finance. It is whether financial institutions, fintech companies, and technology providers can control access to financial data with the discipline, transparency, and accountability that consumer trust requires.

1. AI is becoming more valuable in financial decision-making

Finance is entering a new AI phase

AI is shifting from back-office optimization to front-office guidance. Consumers can increasingly ask natural-language questions about spending, subscriptions, cash flow, debt repayment, investment risk, and long-term goals. For institutions, the same capabilities can improve service, reduce friction, detect anomalies faster, and deliver more personalized experiences.

Why this feels so powerful to users

Financial decisions are personal, emotional, and often complex. AI can act as an interpreter between fragmented financial data and everyday decisions. It can identify patterns a user may miss and translate them into practical next steps. This is where AI becomes not just an efficiency tool, but a behavioral influence engine.

Why the market is rushing in: the “gold rush” dynamic

Banks, fintechs, wealth platforms, payment firms, and technology companies are competing to become the trusted interface for personal finance. The incentive is clear: the institution that becomes the intelligence layer for personal finance may also become the platform that shapes customer relationships, captures deeper financial context, and influences future financial decisions.

2. Privacy risk rises as AI value increases

The core risk: sensitive financial data

Financial data reveals more than balances. It can indicate where people live, work, travel, receive care, donate, borrow, invest, and experience financial stress. When AI analyzes that data, it may generate sensitive behavioral profiles and inferences that consumers do not fully see or understand.

Privacy is not just about breaches — it is about control

The question is not only whether data is stolen. It is also whether data is over collected, retained too long, repurposed, shared across vendors, or used to infer sensitive traits. Meaningful consent becomes harder when AI systems transform raw transactions into predictions, classifications, and recommendations.

Convenience vs. trust

Consumers want personalization, but not at the cost of losing visibility and control. The trust equation will depend on transparent notices, clear permissions, clear controls for disconnecting accounts, data minimization, clear restrictions on how data can be reused beyond the original purpose, and plain-language explanations of what AI can and cannot do.

3. Financial institutions should strengthen controls around AI access to consumer data

Internal IT controls: AI needs accountable oversight from within

As AI becomes embedded into financial workflows, institutions need clear controls over how AI tools are approved, accessed, configured, monitored, and changed. Core IT controls should include role-based access, segregation of duties, change management, audit logging, vendor oversight, incident response, and periodic control testing.

AI-specific controls should go further. Institutions should define what data AI tools can access, which use cases are permitted, how prompts and outputs are monitored, and when human review is required before AI-assisted recommendations or decisions are used. Where AI systems connect to external tools, data sources, or agents through mechanisms such as Model Context Protocol (MCP), institutions should also control tool permissions, restrict unnecessary connectors, validate trusted servers, monitor tool calls, and prevent unauthorized data retrieval or action execution.

Data quality is equally important. AI outputs are only as reliable as the data used to generate them, so institutions should establish controls to confirm that financial data is accurate, complete, current, and traceable to trusted sources before it is used for analysis, recommendations, or customer-facing outputs.

These controls help ensure AI does not operate as an unmanaged “black box.” They create accountability over what data AI can access, how outputs are used, whether the underlying data is reliable, and whether unauthorized activity is detected and addressed in a timely manner.

Third-party risk: finance AI depends on an ecosystem

AI-enabled financial services often rely on AI model providers, cloud platforms, data aggregators, fintech integrations, identity tools, and API-based account connections. Each provider may create another path through which sensitive consumer financial data is accessed, processed, stored, or shared.

This makes third-party risk a core part of AI governance. Institutions need enough visibility into how external providers handle consumer financial data, how AI-related services are supported, and where accountability sits when data is misused, retained beyond its purpose, or exposed through a vendor's environment.

Cybersecurity risk: AI can help defenders, but it also helps attackers

When financial institutions use AI to process customer data, cybersecurity risk is not limited to traditional breaches. The larger concern is that AI introduces new ways for sensitive data to be accessed, processed, retained, or exposed through prompts, logs, API connectors, and third-party platforms.

AI systems often sit between customer records, transaction histories, document repositories, and internal financial systems. If these connections are not properly controlled, adversaries may manipulate prompts, connected data sources, or system instructions to extract sensitive information, distort AI outputs, or cause customers to receive inaccurate guidance. In financial services, that can quickly become more than a technical issue; it can create customer harm, regulatory exposure, and reputational damage.

Institutions should establish AI-specific internal controls and test them regularly. This includes reviewing changes to AI prompts and configurations, validating what data AI tools can access, and checking whether AI responses remain accurate, complete, and appropriate for customer use.

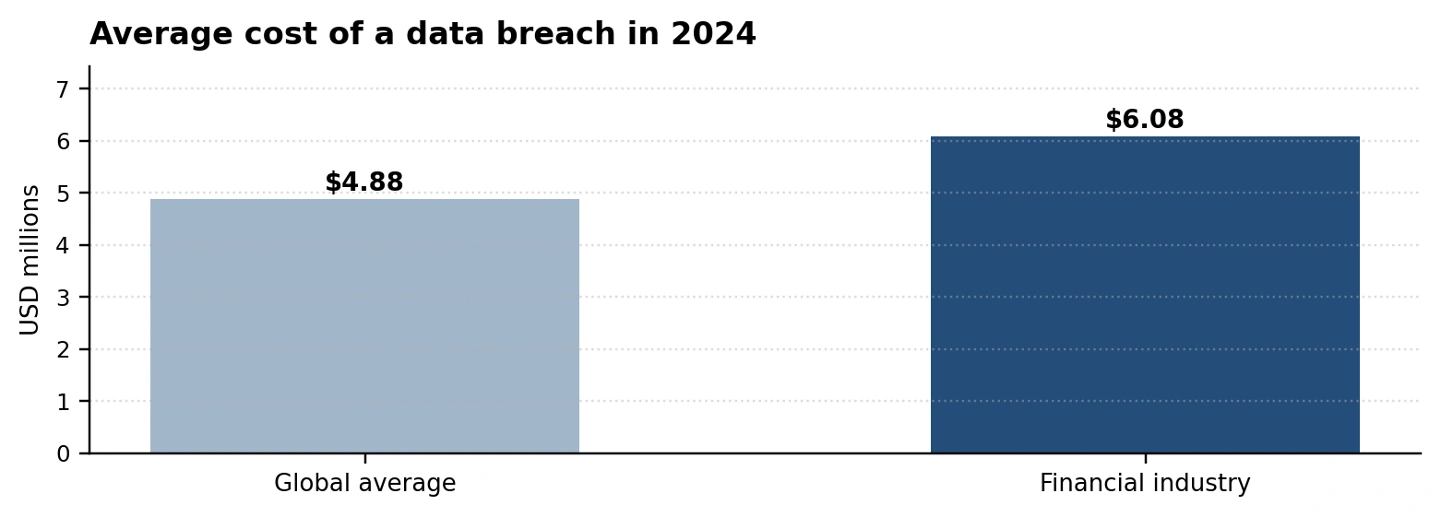

Source: IBM, “Cost of a data breach 2024: Financial industry.” Financial firms averaged USD 6.08M, compared with the global average of USD 4.88M. Link

4. Regulators should move faster to define guardrails for AI-driven financial data access

The governance question: are controls maturing fast enough?

AI adoption in financial services is moving faster than many governance, privacy, and supervisory models. This creates important questions that cannot be left entirely to market practice.

What does meaningful consent look like when AI can turn transaction history into sensitive behavioral insights? How should AI-driven financial recommendations be explained to consumers? When does personalized guidance become regulated advice? Who is accountable when AI vendors, data aggregators, or connected platforms contribute to consumer harm?

These questions matter because AI does not simply process financial data. It can interpret it, enrich it, classify it, and influence how financial decisions are presented to consumers.

Trust and governance as competitive differentiators

Clear guardrails do not need to slow responsible innovation. In financial services, well-defined expectations can help organizations scale AI with greater confidence while giving consumers more visibility into how their financial data is accessed and used.

The organizations best positioned to benefit from AI will not be those that move fastest without structure. They will be those that can show disciplined governance, responsible data use, effective oversight of AI-enabled ecosystems, and accountability when AI affects consumer outcomes.

Practical recommendations

Conclusion: cultivating innovation without planting risk

AI can make financial services more accessible, personalized, and proactive. It can help consumers understand financial decisions, allow organizations to serve customers more effectively, and strengthen how the sector detects fraud, monitors risk, and responds to change.

But consumer financial data is not ordinary data. It can reveal income, debt, spending behavior, health-related payments, investment choices, location patterns, and moments of financial vulnerability. When AI systems access and interpret that data, privacy and security risk expands beyond traditional breaches. It includes overcollection, unclear consent, third-party data movement, unreliable outputs, prompt manipulation, and insufficient control over how customer information is processed, stored, shared, and deleted.

The path forward is not to slow AI adoption in finance. It is to govern it with the discipline financial data requires. Organizations that want to earn trust will need clear data-access policies, tested AI-specific controls, reliable data quality, accountable vendor oversight, and meaningful transparency for consumers.

The AI gold rush in finance is real. Whether it creates durable value or unmanaged exposure will depend on the governance, security, and accountability decisions being made now.

Subscribe to get the future series of the article

Mondaq LinkedinSubscribe for our latest insights

Sign up for more of our thought leadership and analysis—sent straight to your inbox.

Sign Up